Think about how seriously we take mathematics in this country.

Tuition classes from Class 3. Extra practice on weekends. Parents who quietly stress about board exam percentages. Teachers who repeat the same concept five different ways until it clicks. And behind all of it, a completely reasonable belief: maths matters. A child who understands numbers — who can count, calculate, reason, and apply — will be more capable, more employable, more able to navigate the world.

We are right about this. Maths is foundational.

Now ask yourself: how much time does that same child spend learning what to do with the money their maths-enabled career will eventually earn?

For most children growing up in India today, the answer is close to zero. Not because parents don't care — they do, deeply — but because financial literacy has never been treated as a subject that needs to be taught. It is assumed that children will pick it up. From watching. From osmosis. From "figuring it out" when they're older. The NCFE's nationwide survey found that only 27% of Indian adults are financially literate — which means most of that "figuring it out later" isn't working. For a practical starting point on what to actually teach and when, our Complete Parent's Guide to Financial Literacy for Kids in India covers the full picture.

And for a lot of adults, that shows.

This article is about what financial literacy actually is, why starting in childhood produces something qualitatively different from learning it at 30, and what the foundation looks like when it's built right.

Financial literacy is not knowing which mutual fund to pick. It is not understanding CAGR or reading a balance sheet. Those are advanced chapters — useful, eventually, but built on top of something more fundamental.

Financial literacy, at its core, is understanding three things:

What money is. Not coins and notes as objects, but money as a system — a medium of exchange that represents real goods and services produced by real people. A ₹500 note has no intrinsic value. What gives it power is the agreement that it can be exchanged for real things that real people made or did.

How to manage what you earn. Knowing the difference between needs and wants. Making a budget and roughly sticking to it. Saving toward something specific rather than hoping money is left over. Understanding that small consistent choices compound over time.

How money grows — and shrinks. The basics of interest, inflation, investment, and debt. Why idle money loses value. Why compound interest works in your favour when you save and against you when you borrow. Why not all debt is the same.

That is the whole subject. It is not complicated. It is not exclusive to people with finance degrees. It is practical knowledge about something every single person in the world interacts with every single day — and yet almost nobody teaches it to children deliberately.

One parent who used the finance kit put it simply: "Most things out there jump straight to where to invest, which mutual fund to pick, how to build a portfolio. My son is 9 — he doesn't need a portfolio yet. He needs to understand what money actually is. This was the first time he genuinely got it — that money doesn't just appear from a phone or an ATM, that it is a medium of exchange for real goods and services, that someone in our family actually produced something for it to exist. That clarity, at his age, is honestly everything."

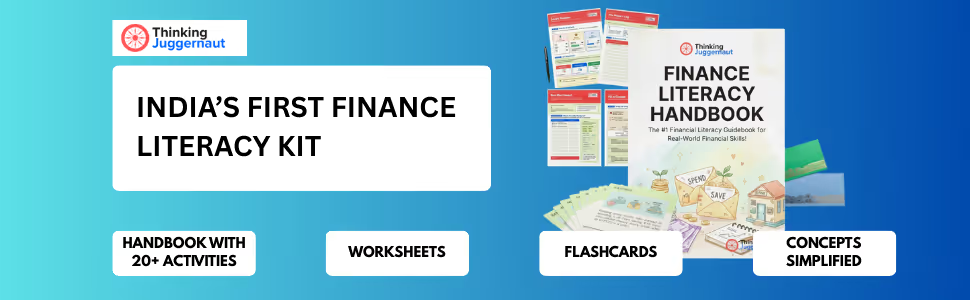

That is exactly what this subject is missing at the foundational level — and what our Thinking Juggernaut Finance Literacy Kit is built to provide.

Here is something worth sitting with.

We spend approximately twelve years teaching children mathematics. We do this because we understand, correctly, that mathematical thinking underlies almost everything that creates value in the modern world. Employability. Problem solving. Business. Technology. Even basic daily life — calculating a bill, comparing prices, understanding a salary slip — requires maths.

So we start early. We build concept by concept. We repeat until it's automatic. We send children to extra classes because we know that fluency in maths comes from exposure over time, not from one lesson before the exam.

Financial literacy is the same subject, one step downstream.

All those years preparing a child to generate value — to get a job, to build a business, to produce goods or services the world will pay for — and almost no time preparing them for what comes next: what to do with the value they generate once they have it.

The child who earns ₹50,000 a month at 24 and has no framework for managing it is not better off than the child who earns ₹35,000 and knows exactly what every rupee is doing. Often they are worse off — because the gap between what they earn and what they feel they should be able to save creates a specific kind of confusion and stress that no one prepared them for.

Financial literacy is not a nice-to-have. It is the second half of the preparation we already believe in — completing the loop from earning to managing well.

Before budgeting. Before saving. Before anything.

The most important thing to establish — with children, at the earliest sensible age — is what money actually represents.

When a parent makes a UPI payment, a child sees a phone tap and then something arriving. The connection between that tap and the work that funded it is invisible. Money appears to come from a device. Things appear to come from a tap. The idea that someone in the family produced goods or services, exchanged that for money, and is now exchanging money for something else — that chain is completely hidden.

When the chain is hidden, money feels like it comes from thin air.

And when money feels like it comes from thin air, a child cannot build a healthy relationship with it. They cannot understand why "we can't afford that" is a real statement rather than a preference. They cannot understand why saving requires giving something up now. They cannot understand why work connects to anything meaningful.

Here is the chain stated simply: your family produces value — a skill, a service, a product, time, expertise. The world pays for that value with money. That money is then used to exchange for other people's value — food, shelter, education, experience. Money is the middle step. It is the agreed-upon medium that makes exchange between strangers possible.

Once a child internalises this, everything else makes sense. Spending is not just a number changing — it is real value, produced by real effort, moving from one place to another. Saving is not just restriction — it is keeping value for your future self. And earning is not just receiving — it is producing something the world finds worth exchanging for.

This is the foundation. It takes one good conversation to plant and a lifetime of small reinforcements to grow.

There is a specific advantage that comes from learning something foundational in childhood rather than adulthood.

When you learn maths at 7, you don't think about maths. You just calculate. The foundation is so deep it becomes invisible — it is simply how your mind works with numbers. You don't have to effort your way through it every time.

Financial literacy works the same way. A child who learns to ask "is this a need or a want?" at 9 will ask that question automatically at 29, without thinking about it, without effort, without needing to remind themselves. A child who learns to save toward a goal at 10 — putting something into an envelope every week, watching it grow toward something specific — has built a habit that is genuinely hard to unlearn.

Over time, with reinforcement, these habits compound. Not dramatically. Just steadily. In ways that become very visible by the time that child is 35.

The adult who starts learning this at 28 can absolutely get there. But they are working against habits already formed, against reflexes already established, against a relationship with money that has years of unexamined history. It is possible. It is just harder and slower than it needed to be.

Starting at 9 means the foundation is just there. Quietly. Automatically. The way arithmetic is.

It is simply true that understanding something protects you from people who rely on your not understanding it.

Scams and manipulation. Every financial scam — every "guaranteed 40% returns" scheme, every fake loan offer, every investment that turns out to be a Ponzi — works because the target does not have a clear enough model of how money actually works. A child who knows that money represents real value, that nothing is genuinely free, that returns always carry risk proportional to their size — that child is not easily taken in. Not at 14. Not at 40.

Predatory marketing. Advertising is designed to make wants feel like needs, to create urgency that overrides reflection, to make you feel behind if you don't buy something. A child who has practised distinguishing needs from wants — who has done it enough times that the question is automatic — is not easily moved by this. They can enjoy advertising without being driven by it.

Their own habits. Money comes in, money goes out, and at the end of the month it is unclear where it went. Financial literacy doesn't solve this by willpower. It solves it by making the system visible and habitual early enough that it never needs to be imposed from outside.

The Thinking Juggernaut Finance Literacy Kit is designed around exactly this sequence — foundation first, concepts second, habits through doing.

The handbook opens with the question every child should be asked: what is money, actually? Not as a definition to memorise, but as a problem to explore. The No-Money Trading Game makes the case through experience — children discover why barter fails and why a medium of exchange had to be invented. Then the evolution from shells to coins to notes to UPI, explained in a way that makes the whole system feel logical rather than arbitrary.

The My Money Log worksheet builds the tracking habit — every rupee in, every rupee out, labelled and totalled. Children doing this for the first time are consistently surprised by their own numbers. The surprise is the lesson.

The Smart Shopper worksheet brings the maths connection to life — comparing prices per unit across different pack sizes, checking whether a BOGO offer is actually a good deal, working with a real shopping budget. These are the calculations that separate informed consumers from impulsive ones.

The Save-Spend envelope system makes money physical in a digital world. When a child splits their pocket money between two envelopes and writes a goal on the Save one, they have made a real financial decision. Not simulated. Real.

The kit further extends this into banking, investing, loans, and inflation — building on the same foundation, with the same hands-on approach, for children ready for the full picture.

For the complete age-by-age guide to what to teach and when, read our Complete Parent's Guide to Financial Literacy for Kids in India.

And for where to start with the most practical first concept — how to teach your child to tell a need from a want — read How to Teach Kids the Value of Money: The Needs vs Wants Guide.

Thinking Juggernaut builds NEP-2020 aligned, hands-on learning kits for children. The Finance Literacy Kit (Age 7+) and Finance Explorer Kit (Age 10+) are built around the belief that children learn finance by doing it — not by reading about it.

Almost there!

We will confirm your order on WhatsApp

Order placed!

Thank you! You will receive a WhatsApp confirmation shortly.

![[background image] electronics workbench](https://cdn.prod.website-files.com/6867e17b7728d4dad1984de4/69a46d2edc56acb459af12aa_What%20is%20true%20finance%20literacy.avif)

![[digital project] image of past client project on a magazine page](https://cdn.prod.website-files.com/6867e17b7728d4dad1984de4/6972ee0bf80a40e0e1fc016a_15.avif)

![[digital project] image of past client project on a magazine page](https://cdn.prod.website-files.com/6867e17b7728d4dad1984de4/69a7c5bdcf3c94ba7fa77bf2_Finance%20Literacy%20Kit%20(Age%209%2B).avif)