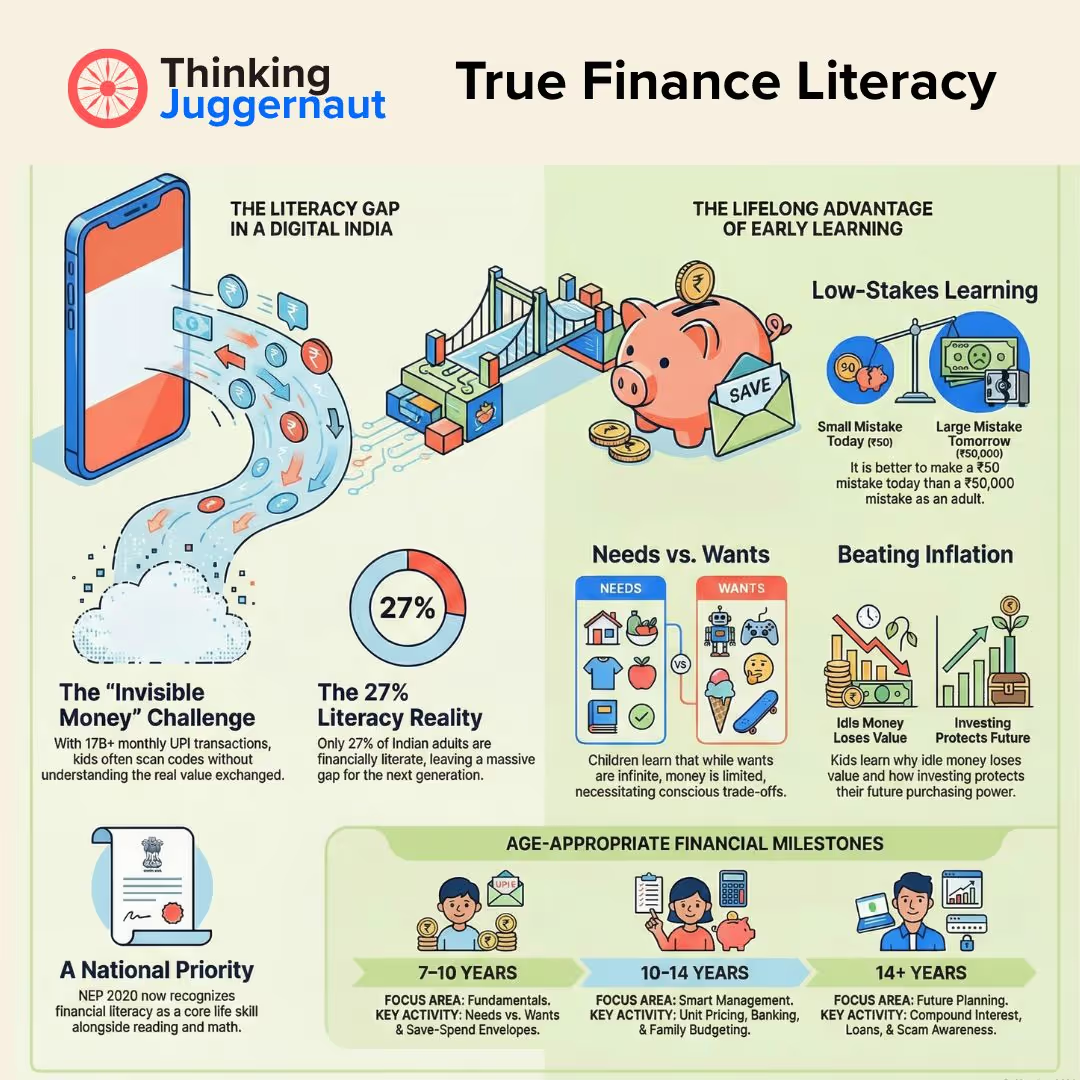

Here is something worth thinking about: your child probably knows how to scan a QR code before they know what the money behind it actually represents.

That's not a problem — it's an opportunity. We live in a remarkable time. UPI, digital wallets, online shopping — India's payment ecosystem is world-class and genuinely convenient. But beneath every tap and scan, real value (goods or services) is exchanging hands. It is essential that kids understands this foundational layer— not just how to pay, but what money is and how it works.

Financial literacy is a life skill and mindset that needs to be cultivated from an early age. According to an RBI survey, only about 27% of Indian adults are financially literate — and for students, that number is even lower. NEP 2020 has tried to promote financial literacy at all levels of education, recognising it as a core life skill alongside reading, writing, and arithmetic.

This guide is your starting point

Before anything else, let's get this right.

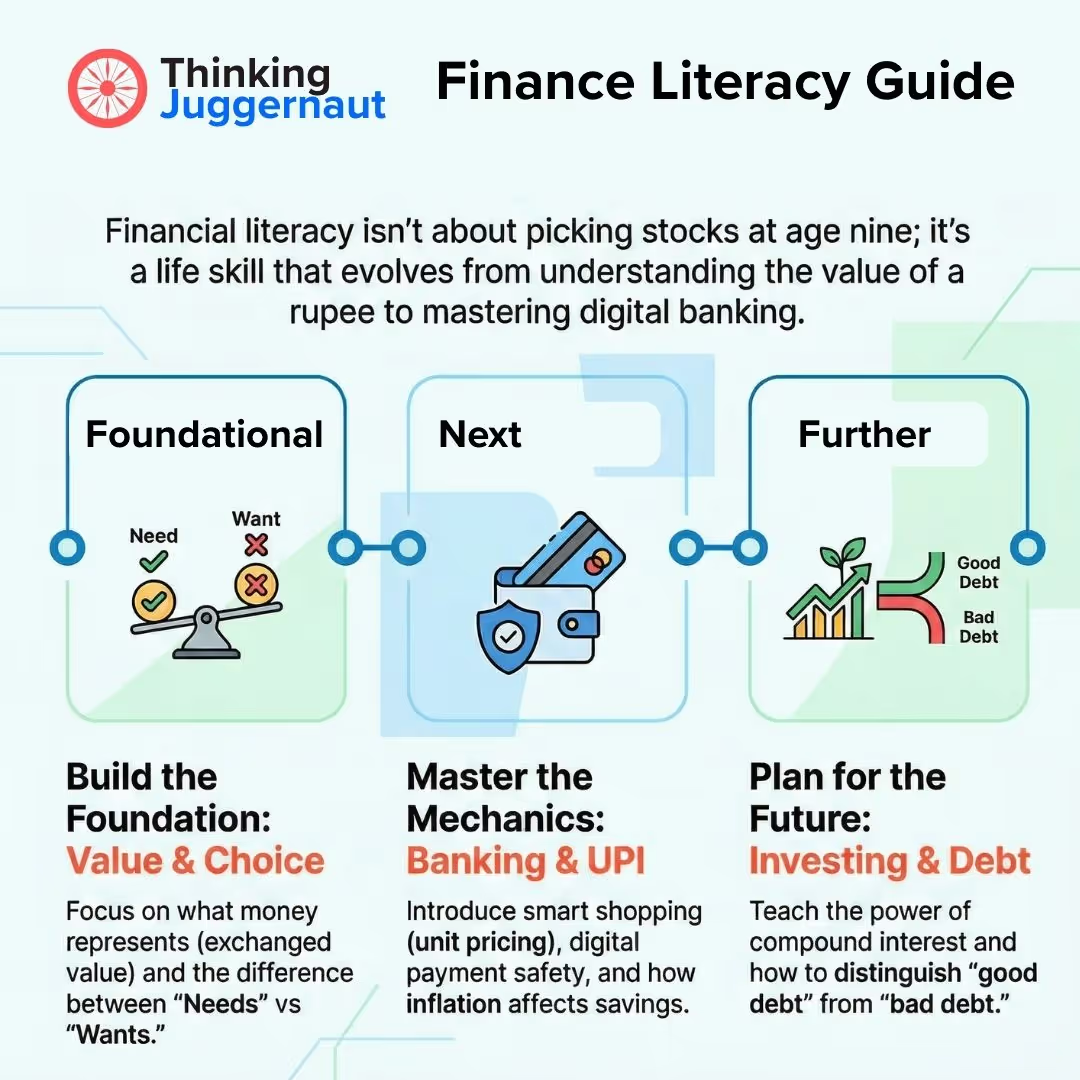

Financial literacy for children is not about teaching which investment type to pick when they grow up. Those are important eventually — but they're the advanced chapters. You don't start a child on calculus before they've done arithmetic.

Real financial literacy, at the right age, starts with the most fundamental question: what is money, actually?

A ₹100 note is a piece of paper. What gives it power is that everyone agrees it represents value — value that came from someone's work, skill, or time. Whether your child pays for something with cash, a debit card, or a UPI scan, the same thing is happening underneath: value is moving from one person to another. Money is simply the agreed-upon medium that makes that exchange possible.

Once a child understands this — once it clicks — something changes in how they relate to it. Suddenly, spending is a choice, not a reflex. Saving is a strategy, not a lecture. And the concept of earning starts to feel real, not abstract.

From there, true financial literacy at the right age means:

That is the foundation. Everything else builds on it. And the best time to lay it is in childhood, when habits form naturally and the cost of a mistake is ₹50, not ₹50,000.

India has just gone through one of the fastest financial transformations of any country in history. Digital payments are mainstream. UPI is processing over 17 billion transactions in single months. Your child is growing up in a world where money flows invisibly and instantly.

This is genuinely exciting — and it makes financial literacy more important, not less. When money is invisible, it's easy to lose the sense of where it comes from and what it costs. The child who understands that every payment — however effortless it looks — represents someone's earned value, is the child who will make better decisions with their own money later.

The RBI collaborated with several State Educational Boards in 2022 to introduce financial literacy modules in school curricula, and NEP 2020 identifies life skills — including financial literacy — as core learning outcomes from the foundational stage onwards. The momentum is building. Parents who start at home give their children a real running start.

If you want to understand what NEP actually changes for your child's school day, we've covered that in detail here.

Financial literacy is not a single conversation — it's a progression. Each concept creates the foundation for the next one.

This is the golden window. Children as old as 7 are old enough to understand these concepts, curious enough to engage, and young enough that habits form easily.

Start with what money actually is. Not coins and notes as objects, but money as a system — a way humans solved the problem of trading value with each other. Try the No-Money Trading Game: ask your child to imagine a world with no money. They have mangoes; they want a notebook. They need to find someone who wants mangoes and has a notebook. Good luck. That's why money was invented. This single conversation — which takes five minutes — gives children a frame they'll carry for life.

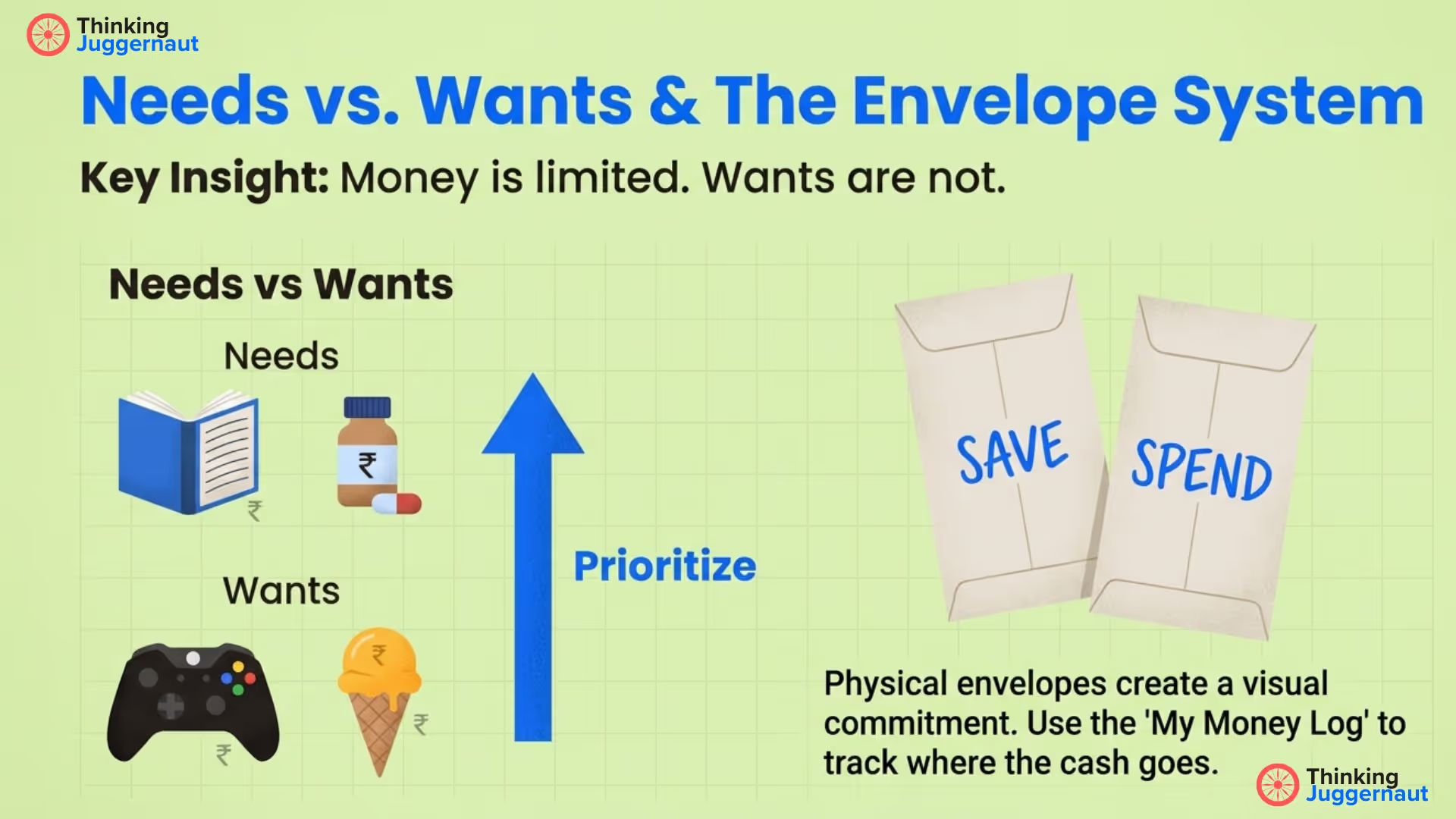

Then introduce needs vs wants. Food, school supplies, medicines — needs. The extra game, the fancy shoes, the second portion of ice cream — wants. Here is the real lesson underneath: money is limited, wants are not. Every purchase is a choice. This is not a lesson to lecture about — it's one to practise. Which is why the Thinking Juggernaut Finance Literacy Kit includes a My Money Log worksheet where children track every rupee they spend and label it Need or Want. When a child sees their own spending in a table — "I spent ₹180 on canteen snacks this month" — no adult needs to explain anything. The data does it.

Introduce the Save-Spend envelope system. Give your child pocket money and two physical envelopes — one labelled Save, one labelled Spend. Ask them to decide how to split it. Ask what they're saving toward. Write the goal on the envelope. This is the moment a savings habit begins. Not from a chapter they read, but from a physical action with real money. The Save-Spend envelope system is included in the kit for exactly this reason.

Once the foundation is covered, now they can handle more layered thinking.

Smart shopping. The Smart Shopper worksheet in the kit has children calculate the price per 100ml across three different juice bottle sizes, figure out the actual saving on a "Buy 1 Get 1 Free" biscuit offer, and check whether ₹120 actually covers a real shopping list. They discover quickly that a bigger pack is not always better value — and that "up to 70% OFF" is not the same as 70% off the thing you wanted. These are skills most adults still lack.

Banking and digital money. Next is to explain what happens underneath: what a savings account is, how the bank uses your money, what interest means (in both directions — earned and paid), what UPI actually does, and critically — what digital safety looks like. The handbook covers ATM cards, net banking, UPI, OTP, and a full section on digital security rules. The Fill a Cheque worksheet teaches the mechanics of a banking instrument — not because they'll write cheques tomorrow, but because understanding financial tools is the first step to not being confused or manipulated by them.

How money grows — and shrinks. This is where a story does more than any explanation. Arjun and Priya both get ₹10,000 as birthday gifts. Arjun keeps it in a piggy bank. Priya puts it in a fixed deposit at 6%. Five years later, Priya has ₹13,382. Arjun still has ₹10,000 — but now that ₹10,000 buys less than it did five years ago, because prices have risen. Arjun didn't just miss out on growth — he actually lost purchasing power. The story is in the handbook. Children remember it.

Run the House — the most eye-opening worksheet. It asks the child to sit with their family's actual monthly income and allocate every rupee: rent, groceries, school fees, electricity, mobile, petrol, medicines, savings. Most children, doing this for the first time, discover that the budget is tighter than they thought. That savings disappears first when other things cost more. That the family's financial life involves dozens of conscious tradeoffs every month. This one activity builds more empathy and financial understanding than any book chapter.

The Thinking Juggernaut Finance Kit goes deeper — A personal finance handbook that covers foundational concepts plus smart shopping, banking in detail, investments, loans, inflation with 20+ activities and along with worksheets, flashcards, and the Save-Spend envelope system.

Investments. The foundation: if you leave money idle, inflation erodes it. A bicycle that costs ₹5,000 today will cost significantly more in five years. Money needs to work. Fixed deposits, recurring deposits, gold — these are the starting rungs. The concept of compound interest — earning interest on interest — is introduced through the handbook's clear step-by-step example, showing exactly how ₹1,000 grows differently under simple vs compound interest over three years.

Loans. Not all debt is equal. A student loan that funds an education which increases earning power is fundamentally different from a personal loan for a gadget. Good debt invests in your future. Bad debt funds temporary wants. Children who understand this before they encounter their first credit card offer are protected in a way that most adults weren't.

Scam awareness. Once you know how money actually works — that it represents real value, that "guaranteed returns" always have a cost somewhere, that free money doesn't exist because someone always did the work — financial scams become much harder to fall for. This isn't about making children anxious. It's about making them fluent enough in the rules that manipulation doesn't work on them.

There are more finance products for children in India than there were two years ago, which is a good thing. But most of them share the same approach: start with investing. Mutual funds, compounding, equity, SIPs. Real concepts, genuinely useful — eventually. But they're chapter 10. If a child doesn't yet understand why they can't have everything they want, teaching them about compounding is like teaching long division before subtraction. The foundation is missing, so the concept floats.

We built the Finance Literacy Kit covering what we discussed so far. What money is. Why you can't have everything. How to make a choice. How to save toward something. How to read a bill. How a bank actually works. The concepts that make everything else make sense — and that most adults quietly wish someone had taught them at 8 instead of 38.

The Finance Literacy Kit (Age 7+) and Finance Explorer Kit (Age 10+) are built around exactly this sequence.

The kit is built around doing, not reading. Experiential learning consistently outperforms passive instruction — across every subject, not just finance.

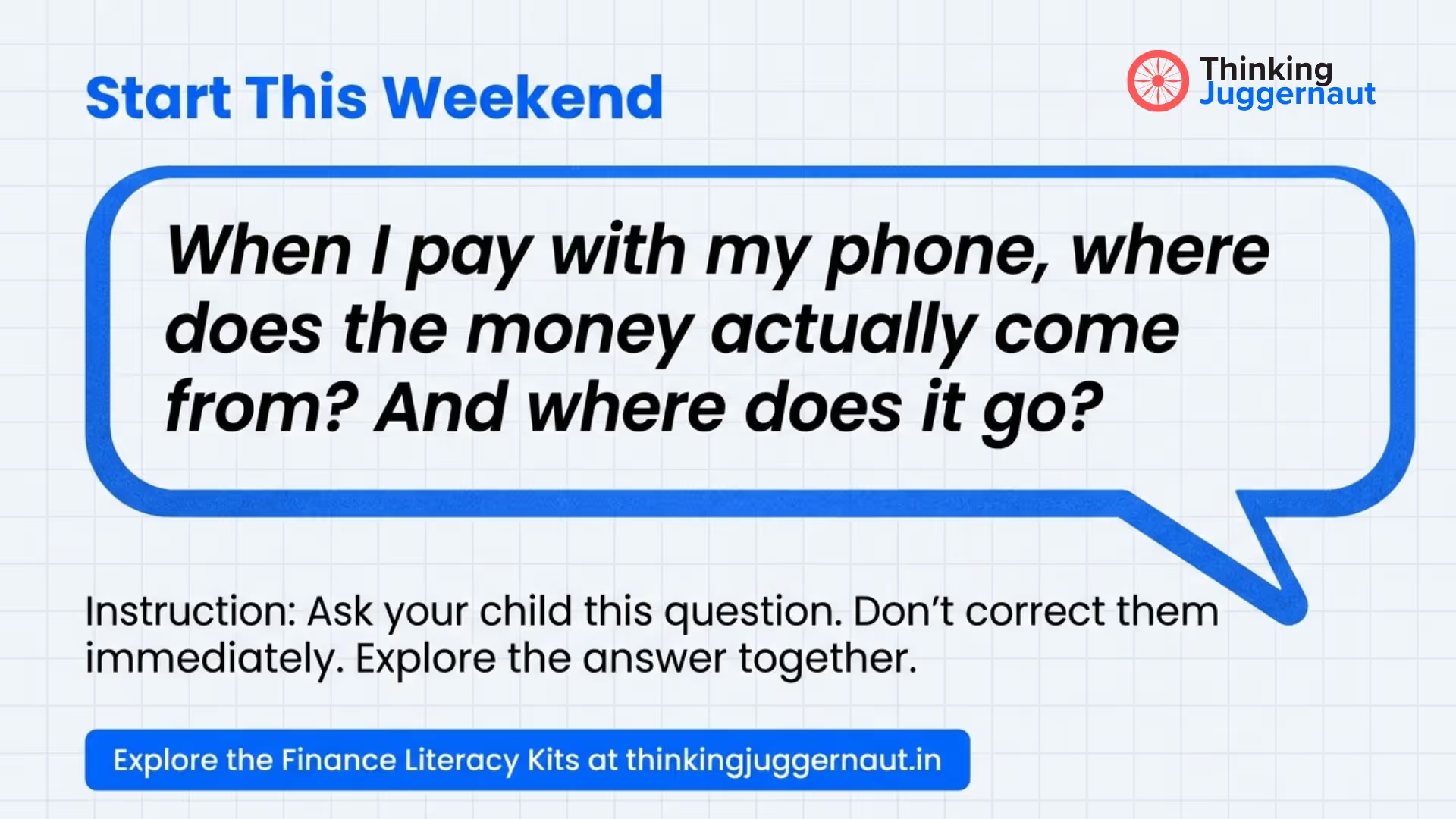

You don't need a lesson plan. Start with one conversation.

Ask your child: "When I pay for something on my phone — where does that money actually come from? And where does it go?"

Let them think. Don't correct immediately. Then explore it together. That conversation — five minutes, no preparation — plants the seed.

If you want a complete structured system that takes your child from "what is money?" all the way through banking, budgeting, investing, and digital safety — with a handbook that guides every step, worksheets that create real practice, flashcards that make concepts stick, and a physical envelope system for daily use — the Finance Literacy Kit is built exactly for that.

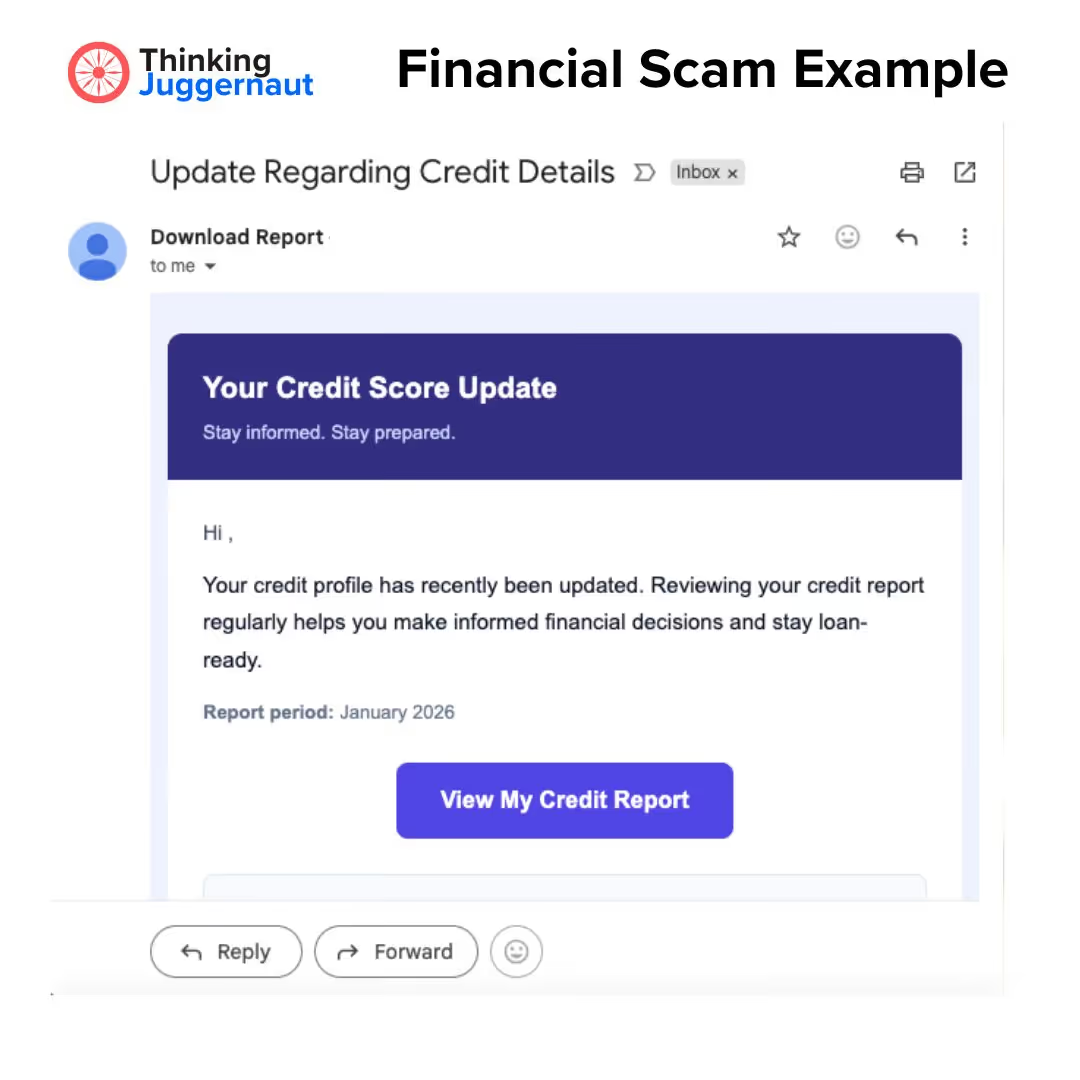

Here is a real email that arrived in a real inbox in January 2026.

Subject line: Your Loan File Number ABPLXXX550 Has Approved Body: "Thank you for submitting your loan request. Your application has been reviewed and the indicative eligibility details are outlined below." Loan Eligibility: Up to ₹5,00,000 Interest Rate: Starting from 10.5%

What is happening here?

"Your Loan File Number... Has Approved" — The grammar is deliberately personal. "Your file." "Your number." It implies you applied for something, that this is a response to your request. In many cases, you didn't apply for anything. The file number is assigned to create a false sense of process — as if approval were almost complete, you just need to confirm.

A child who understands that money represents real work — real goods, real services, real time — reads these emails very differently from one who doesn't. That's the whole point of starting early.

Thinking Juggernaut builds NEP-2020 aligned, hands-on experiential kits for children. Founded by IIT and NIT alumni. The Finance Literacy Kit (Age 7+) and Finance Explorer Kit (Age 10+) are trusted by Indian parents — not because they're the easiest option, but because they actually work.

Almost there!

We will confirm your order on WhatsApp

Order placed!

Thank you! You will receive a WhatsApp confirmation shortly.

![[background image] electronics workbench](https://cdn.prod.website-files.com/6867e17b7728d4dad1984de4/69a7d5f4358f72bc76d4cd76_Needs%20vs%20Wants%20Infographic.avif)

![[digital project] image of past client project on a magazine page](https://cdn.prod.website-files.com/6867e17b7728d4dad1984de4/69a7daf147f8ff5280c02627_How%20to%20Teach%20money%20infographic.avif)

![[digital project] image of past client project on a magazine page](https://cdn.prod.website-files.com/6867e17b7728d4dad1984de4/69a7c5bdcf3c94ba7fa77bf2_Finance%20Literacy%20Kit%20(Age%209%2B).avif)