Every rupee your child spends is a choice. The question is whether they know they're making one.

Think about the last time your child asked for something at a shop — a chocolate, a new game, that one toy they'd been eyeing. And think about what happened when you said no, or not now. Was it a conversation, or was it a battle?

That moment — that exact moment — is where financial literacy begins. Not in a classroom, not in a textbook. Right there at the shop counter.

Needs vs wants is the first and most important money concept a child will ever learn. Get this one right, and everything else — saving, budgeting, smart shopping — builds naturally on top of it. Skip it, and even the best financial habits will feel like rules imposed from outside rather than decisions made from within.

This is not about saying no to everything fun. It is about helping your child understand why choices exist — and how to make them well. If you are just starting out and want the full picture first, read our Complete Parent's Guide to Financial Literacy for Kids in India. And for context on why financial literacy is now a national priority, the NCFE's research on financial literacy in India is worth a look.

The textbook definition is simple enough:

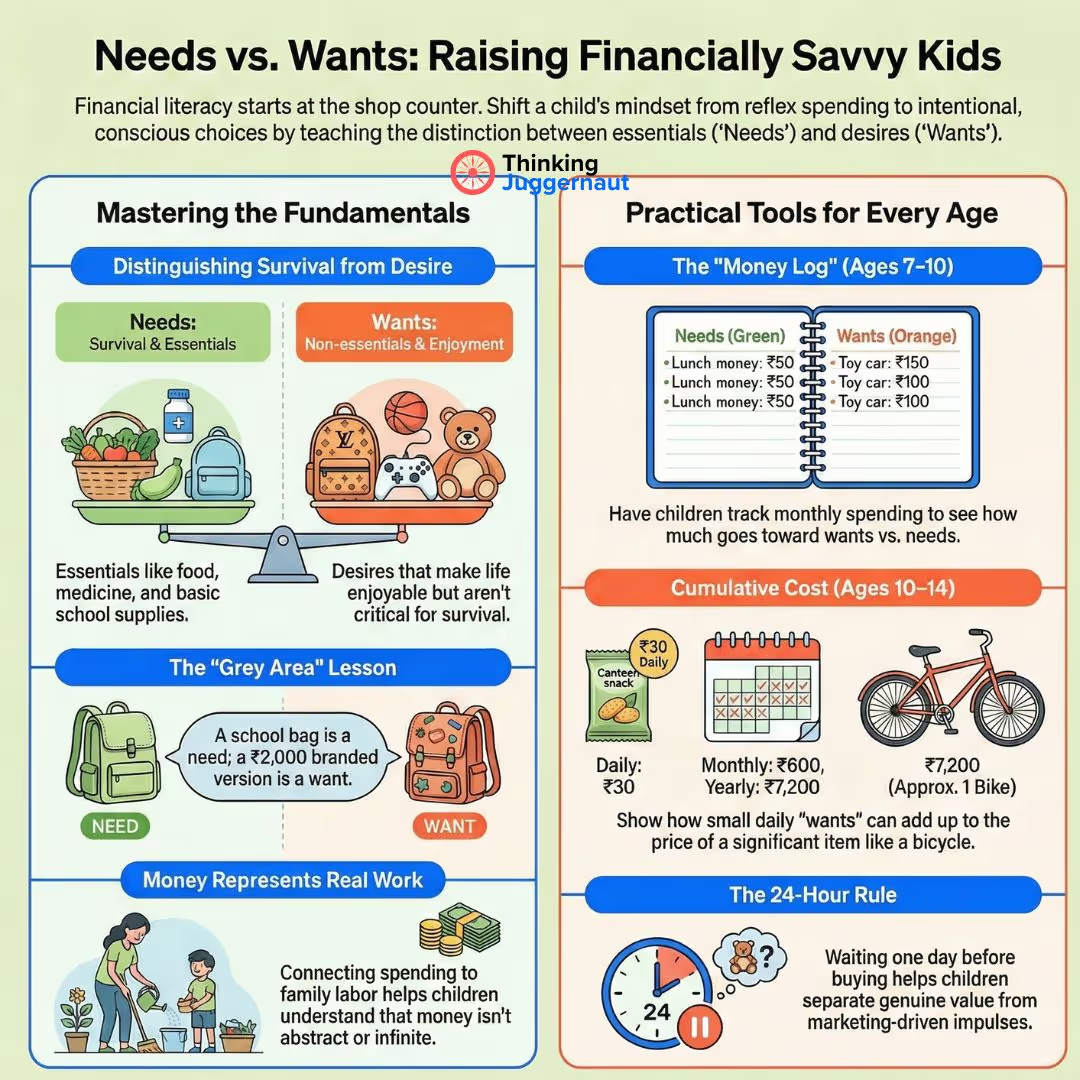

Needs are things required to live and function — food, clothing, shelter, school supplies, medicines.

Wants are things that are nice to have but not essential — the extra game, the fancier shoes when the current ones are fine, the third serving of chaat.

But here is what most explanations miss: the line between needs and wants is not always obvious, and that is exactly the point.

Is a school bag a need? Yes. Is the ₹2,000 branded one when a ₹400 one does the job equally well — need or want? That is where real thinking begins.

Is food a need? Of course. Is the ₹180 café sandwich when there is lunch packed at home — need or want?

The goal is not to give children a rule. The goal is to give them a question they will ask themselves for the rest of their lives: Do I need this, or do I want it?

Once that question becomes automatic, the battle at the shop counter disappears. Not because the child stops wanting things — they won't — but because they start making conscious choices rather than reflex ones.

Here is something worth sitting with for a moment.

When your child asks for something and you pay — whether you hand over cash, tap your debit card, or scan a UPI QR code — what does your child actually see? A phone screen. A beep. The thing arriving.

What they don't see is the work that produced the money in the first place.

Your salary exists because you produced goods or services that someone was willing to pay for. A doctor earns because they provide health. An engineer earns because they solve problems. A shopkeeper earns because they make things available. Every rupee in your wallet or your UPI balance represents real work that someone did — most likely you.

This is the single most important thing a child can understand about money: it doesn't appear from thin air. Whether it comes as cash from an ATM, a Swiggy delivery that arrives in 30 minutes, or a toy ordered online that shows up the next day — behind every single one of those transactions, a real person did real work.

When a child truly internalises this, wants and needs start to feel different. Spending stops being abstract. And saving starts making sense — because saving means your future self gets to use the value that present you worked for.

A conversation worth having with your child: "When I pay for something, where did that money come from? What work did our family do to earn it?"

You don't need to make it heavy. Just make it real.

At this age, start with clear examples — food is a need, a video game is a want — and then introduce one that isn't obvious.

Try this: next time you're at a grocery store or a kirana shop, pick up two items. One is clearly a need (rice, dal, toothpaste). One is clearly a want (a packet of fancy biscuits, a juice box). Ask your child which is which. Easy so far.

Then pick one that's ambiguous — a chocolate milk carton, a branded version of something you usually buy generic. Is this a need or a want? Watch them think. That thinking is the lesson.

The My Money Log worksheet in the Thinking Juggernaut Finance Literacy Kit is built exactly for this age. Children track every rupee they spend — canteen snacks, stationery, a gift for a friend — and mark each one N (need) or W (want). At the end of the month, they add up both columns.

Most children, seeing their own data for the first time, are genuinely surprised. "I spent ₹220 on wants this month?" The data teaches the lesson better than any parent could.

.avif)

At this age, children can handle numbers and projections. Show them what small, frequent wants add up to.

₹30 on canteen snacks every school day = ₹600 a month = ₹7,200 a year.

That's a bicycle. That's a phone upgrade. That's a trip somewhere.

This is not about guilt. It is about awareness — that small daily wants have a cumulative cost that often surprises people. Adults included.

A good question for this age: "If you saved half your canteen money every day for three months, what could you buy with it?" Let them calculate. Let them decide if the daily snack is worth more than the thing they could save for.

Here is where a lot of financial advice for children goes wrong: it becomes preachy. Say no to wants. Save everything. Don't spend on unnecessary things.

That is not real life — and children know it isn't.

The goal is not to eliminate wants. Wants are what make life enjoyable. The goal is moderation and awareness — knowing that a want is a want, choosing it consciously, and making sure it doesn't crowd out what actually matters.

Eating ice cream is fine. Eating ice cream every day because you never thought about it is different from eating ice cream on Friday as a deliberate, enjoyable treat.

The difference is not the ice cream. It is the choice.

When your child understands that choosing a want is perfectly okay — as long as it is a conscious choice and not just a reflex — financial discipline stops feeling like deprivation and starts feeling like control. That shift is everything.

So the conversation is not "you can't have that." It is: "Do you want that, or do you really want that? And if you buy it, what are you choosing not to buy?"

You don't need a kit or a worksheet to start. You need ₹100 and two envelopes.

The Needs vs Wants Sort:

Give your child a small amount — ₹50 to ₹100, whatever is realistic. Then give them a list of 8–10 things they could spend it on. Mix needs and wants, clear and ambiguous.

Ask them to sort the list into needs and wants. Then ask them to decide how to spend their ₹100 — and which wants they would include if they had money left after needs.

Watch what they choose. Don't correct. Ask them to explain their reasoning.

The conversation that follows is worth more than any explanation you could give.

If you want a structured version of this — finance literacy handbook with 20+ activities, with a money log worksheet, a smart shopping worksheet, and the Save-Spend envelope system all included — the Finance Literacy Kit (Age 7+) and Finance Explorer Kit (Age 10+) are built around exactly this sequence.

Every child, at some point, will say: "But I want it."

That is not a problem. That is the lesson.

And every Indian parent, at some point, will hear the harder version: "But my friend has the same one."

This is where needs vs wants gets genuinely tested — because now it isn't just about the item, it is about belonging, about social comparison, about not feeling left out. That is a real feeling and it deserves to be taken seriously.

The answer is not "we are not your friend's family." That shuts the conversation down. The better response is to make the comparison visible: "Your friend's family made a choice to buy that. We make our own choices about what matters to us. What would you give up to have it?" Sometimes the child will decide it genuinely matters enough. Sometimes, when they think about the tradeoff, they won't. Either way, they made a conscious decision — which is exactly the point.

This is also worth saying plainly to your child, especially as they get older: the world will constantly show them things that look like needs. A new phone that everyone has. A brand of shoes that signals something. A gadget that feels essential. Marketing exists to make wants feel like needs — to create urgency, to manufacture social pressure, to make you feel behind if you don't have something. A child who has genuinely internalised the difference between a need and a want is not easily manipulated by this. That awareness is worth far more than the cost of any kit or conversation.

A few more things that help when they push back:

Don't argue about the specific item. The argument is never really about the chocolate or the toy. It's about the feeling of not getting what they want. Acknowledge that first. "I know you want it. That makes sense."

Bring it back to the choice. "If we buy this, we won't have money for X this week. Which matters more to you?" Let them make the tradeoff consciously.

Use the 24-hour rule for bigger wants. If they still want something the next day, it has more genuine value to them than an impulse. This is one of the smartest personal finance habits adults use — and it works at 9 too.

Connect wants to earning. If they want something that isn't in the budget, help them think about how they could contribute toward it — small tasks, saving pocket money, trading something they no longer use. When they earn toward a want, they value it completely differently.

Here is something worth saying clearly: your child will not get this perfectly after one conversation. Neither will they after two. And that is completely fine — because repetition is how this lesson actually works.

Every time a want comes up and you ask "need or want?", that question gets a little more automatic. Every time they track their spending and see their own data, the awareness deepens. Every time they wait 24 hours and realise they didn't actually want the thing that badly — the muscle gets stronger. Reinforcement over time is the whole point.

And the stakes get higher as they grow. At 8, the difference between a conscious choice and an impulse is ₹50. At 22, it is a credit card bill. At 35, it is whether they have savings when something goes wrong.

Think about what this skill actually protects them from across a lifetime:

Marketing designed to manufacture need. Every advertisement, every flash sale, every "limited time offer" is built to make a want feel urgent and necessary. A child who genuinely knows the difference is not easily moved by this. They can enjoy a sale without being driven by it. They can see a product and evaluate it clearly rather than feel it.

Financial pressure when income changes. A job loss. A business going through a slow year. A medical emergency that reshapes the budget. The ability to look at your expenses and quickly identify what is genuinely necessary versus what can be paused — that is a survival skill. Adults who have never practised this find it almost impossible to do under stress. Adults who learned it young do it almost automatically.

Keeping up with everyone else indefinitely. The "but my friend has the same" conversation does not end at 10. It continues at 25 when colleagues are buying cars, at 32 when everyone seems to be renovating their homes. The child who learns early that other people's choices are not the measure of their own needs is the adult who builds wealth quietly while others wonder where their money went.

None of this requires making money a source of anxiety. It requires making it a subject of awareness — normal, regular, matter-of-fact awareness, like knowing what you eat or how much you sleep.

For a complete, step-by-step guide to financial literacy for your child — from what money actually is, through banking, budgeting, and growing money — read our Complete Parent's Guide to Financial Literacy for Kids in India.

Thinking Juggernaut builds NEP-2020 aligned, hands-on learning kits for children. The Finance Literacy Kit (Age 7+) and Finance Explorer Kit (Age 10+) cover needs vs wants, saving, banking, smart shopping, and growing money — through activities children actually do, not just read about.

Almost there!

We will confirm your order on WhatsApp

Order placed!

Thank you! You will receive a WhatsApp confirmation shortly.

![[background image] electronics workbench](https://cdn.prod.website-files.com/6867e17b7728d4dad1984de4/69a7df2a6148d83382888e76_what%20is%20fin%20literacy.avif)

![[digital project] image of past client project on a magazine page](https://cdn.prod.website-files.com/6867e17b7728d4dad1984de4/6972ee0bf80a40e0e1fc016a_15.avif)